The article under is from a current version of Bitcoin Journal PRO, Bitcoin Journal’s premium markets e-newsletter. To be among the many first to obtain these insights and different on-chain bitcoin market evaluation straight to your inbox, subscribe now.

Disinflation And Financial Coverage

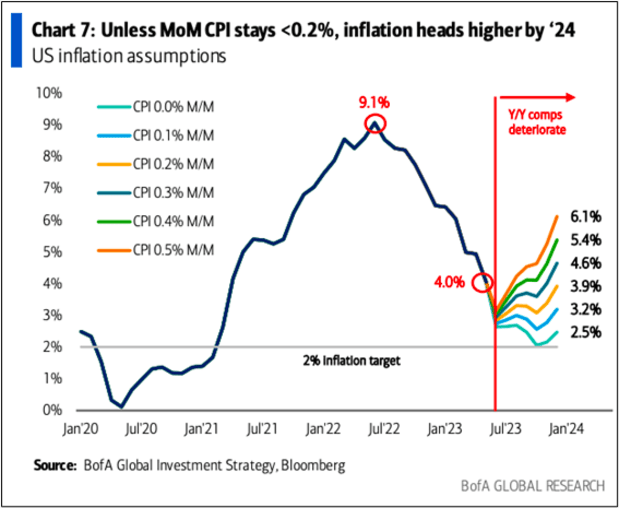

As we delve deeper into 2023, the U.S. financial system finds itself at a crossroads. Disinflation appears to be setting in as a direct results of the Federal Reserve’s tightening financial insurance policies. This coverage shift has led to a notable slowdown within the annualized sticky Shopper Worth Index (CPI) over current months. With this in view, the dialog amongst market contributors has regularly shifted away from inflationary issues and towards attempting to know the influence of the tightest financial coverage in a decade and a half.

The excessive inflation we’ve skilled, notably within the core basket (excluding meals and vitality), hid the results of the swiftest tightening cycle in historical past. Inflation was partially fueled by a good labor market resulting in elevated wages, and leading to a sustained second-half inflationary impulse pushed extra by wages than by vitality prices.

It’s price noting that the bottom results for year-over-year inflation readings are peaking this month. This might result in a reacceleration of inflationary readings on a year-over-year foundation if wage inflation stays sticky or if vitality costs resurge.

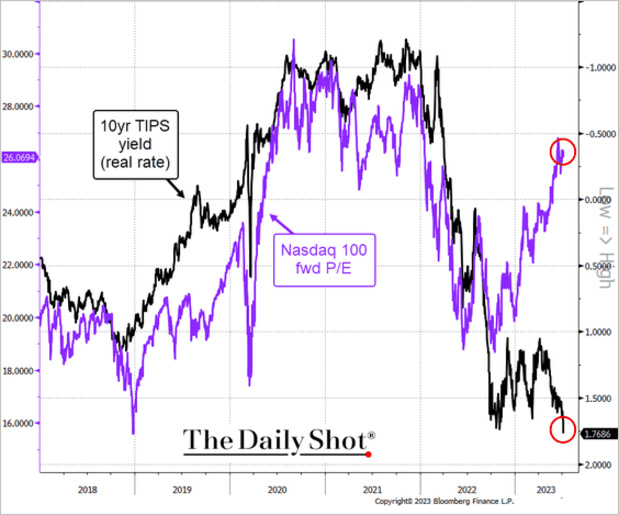

Apparently, actual yields — calculated with each trailing 12-month inflation and ahead expectations — are at their highest in many years. The modern financial panorama is notably totally different from the Nineteen Eighties, and present debt ranges can not maintain constructive actual yields for prolonged intervals with out resulting in deterioration and potential default.

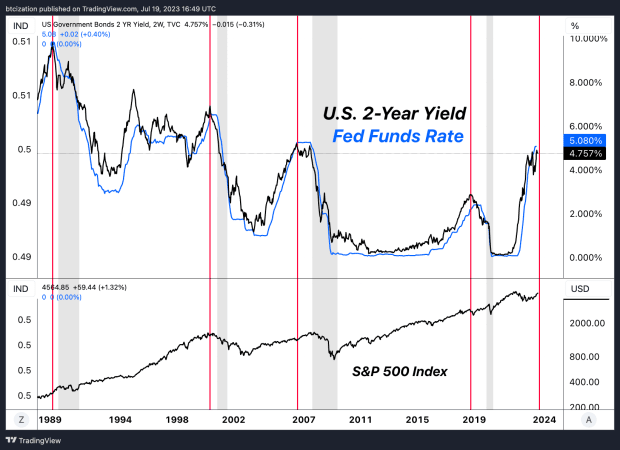

Traditionally, main shifts available in the market happen throughout Fed tightening and slicing cycles. These shifts typically result in misery in fairness markets after the Fed initiates charge cuts. This isn’t intentional, however fairly the unintended effects from tight financial coverage. Analyzing historic developments can present priceless insights into potential market actions, particularly the two-year yields as a proxy for the common of the following two years of Fed Funds.

Bonds And Equities: The Rising Disconnect

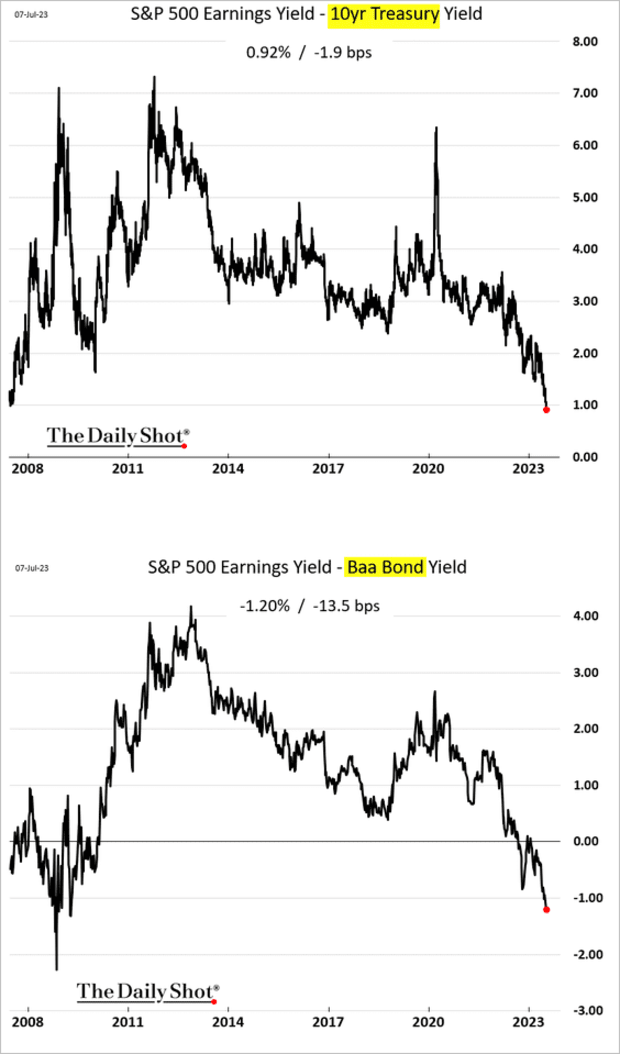

At present, there’s a large and rising disconnect between bond and fairness markets. It’s common for fairness earnings to outperform bonds throughout an inflationary regime as a consequence of equities’ superior pricing energy. Nonetheless, with disinflation in movement, the rising divergence between fairness multiples and actual yields turns into a vital concern. This divergence can be noticed by means of the fairness danger premium — fairness yields minus bond yields.

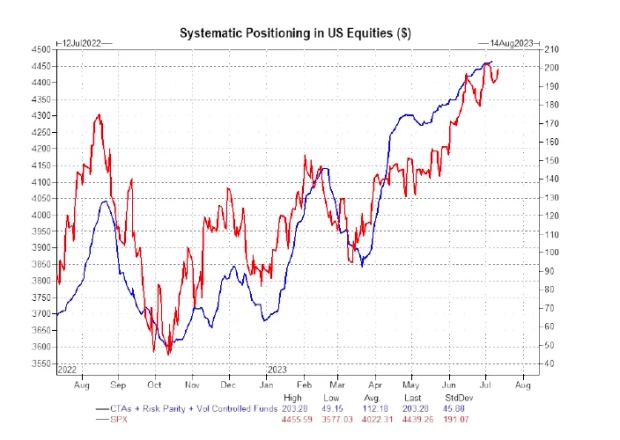

Analysis from Goldman Sachs exhibits systematic funding methods, specifically Commodity Buying and selling Advisors (CTA), volatility management and risk-parity methods, have been more and more utilizing leverage to amplify their funding publicity. This ramp-up in leveraging has are available tandem with a constructive efficiency in fairness indices, which might be pressured to unwind throughout any strikes to the draw back and/or spikes in volatility.

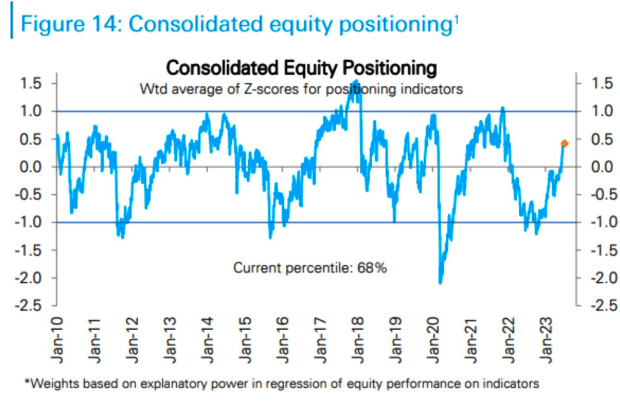

Analysis from JPMorgan Chase exhibits their consolidated fairness positioning indicator is within the 68th percentile, that means equities are overheated, however continuation increased is feasible in comparison with historic requirements.

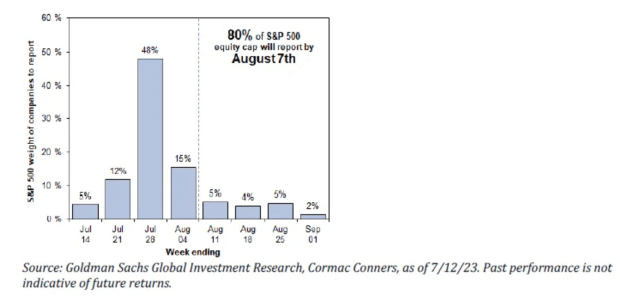

The destiny of fairness markets within the short-to-medium time period can be decided by earnings, with 80% of S&P 500 firms set to finish their reporting by August 7.

Any disappointment throughout earnings season may result in a reversion in fairness valuations relative to the bond market.

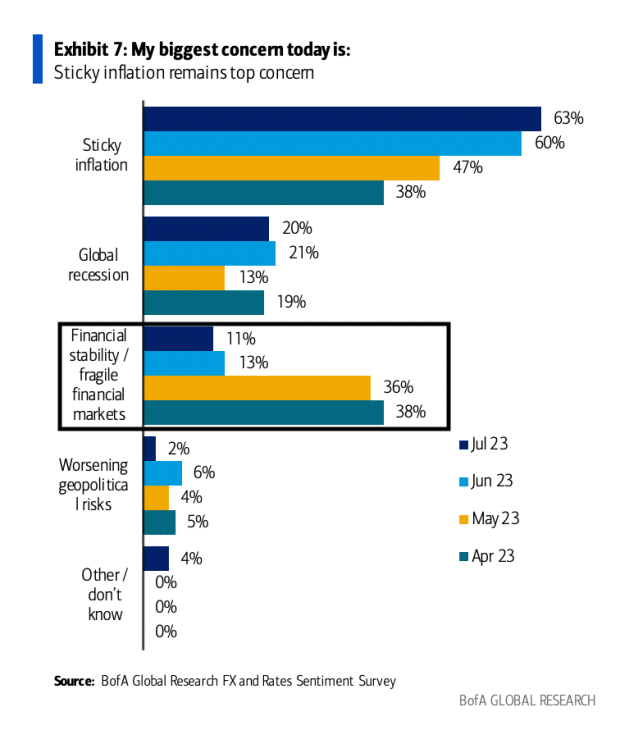

One other attention-grabbing be aware is from a current Financial institution of America survey, the place consumer concern across the well being of monetary markets has risen in current months concurrently fairness markets proceed their uptrend.

Headwinds Forward For The U.S. Shopper?

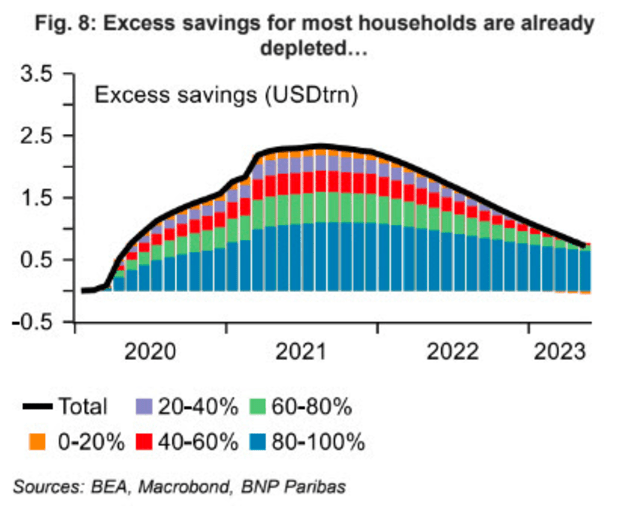

The sturdy earnings surprises and the U.S. shopper market’s resilience are being underpinned partly by extra financial savings from the COVID-era fiscal stimulus. Nonetheless, it’s price noting that these financial savings aren’t uniformly distributed. A current BNP Paribas report estimates that the highest earnings quintile holds simply over 80% of the surplus financial savings. The financial savings of the lower-income quintiles are already spent, with the center quintile seemingly following go well with quickly. With components just like the resumption of pupil debt obligations and rising weaknesses within the labor market, we should always brace ourselves for potential stress in shopper markets.

Regardless of potential shopper market stressors, the efficiency of the U.S. financial system in 2023 has surpassed expectations. Fairness markets have placed on a stellar present, with the bull market showing unrelenting. Amidst these market celebrations, we should keep a balanced perspective, understanding that the trail ahead is probably not as clear minimize or simple because it seems.

Last Be aware

We spotlight developments in fairness and rate of interest circumstances as we discover it essential to acknowledge the rising liquidity interaction between bitcoin and conventional asset markets. To place it plainly:

It indicators substantial demand when the world’s largest asset managers are competing to launch a monetary product that gives their shoppers publicity to bitcoin. These future inflows into bitcoin, predominantly from these presently invested in non-bitcoin property, will inevitably intertwine bitcoin extra carefully with the risk-on/risk-off flows of worldwide markets. This isn’t a detrimental growth; quite the opposite, it’s a development to be embraced. We anticipate bitcoin’s correlation to risk-on property within the conventional monetary markets to extend, whereas outperforming to the upside and in a risk-adjusted method over an extended timeframe.

With that being stated, turning again to the principle content material of the article, the historic precedent of great lag in financial coverage, mixed with the present circumstances within the rate of interest and fairness markets does warrant some warning. Conventionally, fairness markets decline and a technical recession happens in the US after the Fed begins to chop rates of interest from the terminal degree of the tightening cycle. We haven’t reached this situation but. Subsequently, although we’re extraordinarily optimistic in regards to the native supply-side circumstances for bitcoin in the present day, we stay alert to all potentialities. Because of this, we stay open to the thought of potential downward strain from legacy markets between now and mid-2024, a interval marked by key occasions such because the Bitcoin halving and attainable approval of a spot bitcoin ETF.

That concludes the excerpt from a current version of Bitcoin Journal PRO. Subscribe now to obtain PRO articles straight in your inbox.